(400 x 300 px) (1)")

If you’re comparing a mortgage broker vs bank, you’re already asking the right question. Choosing how you arrange your home loan can have a long-term impact on your interest rate, loan features, approval speed, and overall borrowing experience.

This guide breaks down the real differences between using a mortgage broker and going directly to a bank, so you can decide which option best suits your situation.

Mortgage Broker vs Bank: The Key Differences

At a high level, the difference comes down to choice and representation.

A bank offers its own home loan products and works in the bank’s interests.

A mortgage broker compares loans from multiple lenders and works on your behalf.

Both can help you secure a home loan, but the experience and outcome can be very different.

Cost, Choice, Speed & Service Compared

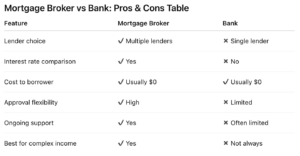

1. Choice of Lenders

-

Bank:

You’re limited to that bank’s products, rates, and lending policies. -

Mortgage Broker:

Access to dozens of lenders, including major banks, smaller banks, and specialist lenders.

Winner: Mortgage broker

2. Interest Rates & Loan Features

-

Bank:

Rates and features are fixed to that bank’s range. -

Mortgage Broker:

Ability to compare interest rates, fees, offsets, redraws, and fixed/variable options across lenders.

Winner: Mortgage broker

3. Cost to You

-

Bank:

No direct fee, but limited choice can mean a higher long-term cost. -

Mortgage Broker:

Usually no upfront cost to you, the broker is paid by the lender after settlement.

Winner: Draw (but brokers often save money long term)

4. Approval Speed & Flexibility

-

Bank:

Standard processes, limited flexibility for non-standard scenarios. -

Mortgage Broker:

Can place your application with the lender most likely to approve you quickly based on your profile.

Winner: Mortgage broker (especially for complex cases)

5. Service & Support

-

Bank:

Staff may change, and service can end once the loan settles. -

Mortgage Broker:

Ongoing support before, during, and after settlement, including refinancing reviews.

Winner: Mortgage broker

Mortgage Broker vs Bank: Pros & Cons Table

When a Mortgage Broker Is the Better Option

A mortgage broker is often the smarter choice if you:

-

Want to compare multiple loan options, not just one bank

-

Are a first home buyer and want guidance through the process

-

Are self-employed, contract, or have variable income

-

Need help navigating lender policies, not just interest rates

-

Want long-term support, not a one-off transaction

In these situations, working with an experienced mortgage broker can significantly improve both approval outcomes and loan suitability.

When Going Direct to a Bank May Make Sense

A bank may suit you if:

-

You already know exactly which loan you want

-

Your financial situation is very straightforward

-

You’re comfortable comparing loans on your own

-

You already have strong banking relationships and discounts

Even then, many borrowers still use a broker to validate their choice before committing.

Final Verdict: Mortgage Broker vs Bank

When comparing mortgage broker vs bank, the deciding factor is usually choice and representation.

Banks represent their own products.

Mortgage brokers represent you.

For most Australian borrowers, especially those wanting competitive rates, flexibility, and expert guidance, a mortgage broker offers broader options and better long-term value.

Learn more about working with a mortgage broker and explore your home loan options with confidence.

Learn more about working with a mortgage broker and explore your home loan options with confidence.

Meet Chris

Chris Berry

Owner of Find A Better Rate Home Loans

Hi, I’m Chris Berry, an independent mortgage broker with over 18 years of experience helping Australians make confident, informed home loan decisions.

I’m the founder of Find A Better Rate Home Loans, where I specialise in assisting first home buyers, refinancers, investors, and self-employed borrowers. With access to 40+ lenders, I compare options across the market to find loan solutions that genuinely suit each client’s situation, not just the most convenient option.

My approach is straightforward: clear explanations, honest advice, and hands-on support from start to finish. I focus on educating clients, cutting through jargon, and making the lending process as smooth and stress-free as possible.

If you’re looking for experienced, unbiased guidance and a broker who puts your interests first, I’d be happy to help.

Our Reviews

We pride ourselves on being brokers you can actually trust, from the initial consultation through to annual reviews that we perform years after your settlement, our tailored services and relationship focus is built to last.

Need proof that we are one of Melbourne’s best mortgage brokerages? Don’t just take our word for it – we have hundreds of positive Google reviews from real clients so you can rest assured you’re making the right choice with choosing Find A Better Rate Home Loans.

Frequently Asked Questions

Get in Touch

98% Approval Rate

18 Years Experience

18 Years Experience

98% Approval Rate

Latest Articles from Find A Better Rate

-

Is Refinancing Still Worth It in 2026? | Australia Guide

A Practical Australian Guide to Refinance Decisions Refinancing a home loan has never been just about chasing the lowest interest rate. It is a decision that involves costs, loan structure, lender rules, and your personal plans. In 2026, many Australian borrowers are reviewing loans taken out in a very different rate environment. At the same…

-

Aussie home owners just got $82,000 richer on average

What a way to start the new year! After a strong 12 months in the property market, plenty of homeowners around the nation are now a whole lot wealthier. And their newfound increase in home equity has opened up some exciting possibilities for 2026. Your home isn’t just a place to live in, it could…

-

Happy New Year! Let’s discuss some potential 2026 goals

There’s nothing quite like a New Year’s resolution to fire you up for another lap around the sun. Whether you’re looking to buy your first home, save on your mortgage, or leverage the equity in your current position, here are three resolutions to consider for 2026. So long, 2025 … You know what? We’ve got…

-

Is Refinancing Still Worth It in 2026? | Australia Guide

A Practical Australian Guide to Refinance Decisions Refinancing a home loan has never been just about chasing the lowest interest rate. It is a decision that involves costs, loan structure, lender rules, and your personal plans. In 2026, many Australian borrowers are reviewing loans taken out in a very different rate environment. At the same…

-

Aussie home owners just got $82,000 richer on average

What a way to start the new year! After a strong 12 months in the property market, plenty of homeowners around the nation are now a whole lot wealthier. And their newfound increase in home equity has opened up some exciting possibilities for 2026. Your home isn’t just a place to live in, it could…

-

Happy New Year! Let’s discuss some potential 2026 goals

There’s nothing quite like a New Year’s resolution to fire you up for another lap around the sun. Whether you’re looking to buy your first home, save on your mortgage, or leverage the equity in your current position, here are three resolutions to consider for 2026. So long, 2025 … You know what? We’ve got…

-

Season’s greetings! Here’s to a well-earned summer break

As the Christmas and New Year’s festive season rolls around, we want to take a moment to sincerely thank you for your trust and support throughout 2025. Fortunately, we had a bit more to smile about this year, with three RBA rate cuts and national property prices increasing by 8.7%. That said, 2025 wasn’t without its…

-

Is Refinancing Still Worth It in 2026? | Australia Guide

A Practical Australian Guide to Refinance Decisions Refinancing a home loan has never been just about chasing the lowest interest rate. It is a decision that involves costs, loan structure, lender rules, and your personal plans. In 2026, many Australian borrowers are reviewing loans taken out in a very different rate environment. At the same…

-

Aussie home owners just got $82,000 richer on average

What a way to start the new year! After a strong 12 months in the property market, plenty of homeowners around the nation are now a whole lot wealthier. And their newfound increase in home equity has opened up some exciting possibilities for 2026. Your home isn’t just a place to live in, it could…

Secure Competitive Home Loan Rates with Trusted Mortgage Lenders

Select from 35+ Trusted Lenders and Tailored Home Loan Solutions