(400 x 300 px) (1)")

Low Deposit Home Loans in Australia Explained

Low Deposit Home Loans are designed to help Australians purchase property with a smaller upfront deposit than traditional home loans. Instead of saving the typical 20% deposit, many borrowers can access Low Deposit Home Loans with deposits as low as 5%, and in some cases even lower depending on eligibility and government support programs.

For many buyers, particularly low deposit home loans for first home buyers, this can significantly shorten the time it takes to enter the property market. Instead of waiting years to save a large deposit, borrowers may be able to secure home loans with low deposit requirements and begin building equity sooner.

However, understanding how these loans work — including lender requirements, loan structure, and potential costs — is essential before applying.

What Are Low Deposit Home Loans?

Low Deposit Home Loans are mortgage products that allow borrowers to purchase property with a smaller deposit than the traditional 20%.

Typically, borrowers can access:

-

5% deposit home loans

-

10% deposit home loans

-

Government-supported low deposit home loans for first home buyers

Because the deposit is smaller, lenders take on greater risk. As a result, lenders often require additional protection, typically through Lenders Mortgage Insurance (LMI) or government guarantee schemes.

Nevertheless, these loans make it possible for many Australians to buy property earlier.

How Low Deposit Home Loans Work

Low Deposit Home Loans work similarly to standard home loans, with the key difference being the size of the deposit required.

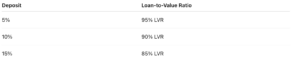

Deposit Requirements for Low Deposit Home Loans

Most lenders require one of the following deposit levels:

The Loan-to-Value Ratio (LVR) represents the percentage of the property value being borrowed.

For example:

Property price: $600,000

5% deposit: $30,000

Loan amount: $570,000

Because the loan represents a higher percentage of the property value, lenders may require additional conditions.

Low Deposit Home Loans for First Home Buyers

Low deposit home loans for first home buyers are one of the most common ways Australians enter the property market.

Many lenders offer products designed specifically for first home buyers who may not yet have a large deposit saved.

Government Schemes Supporting Low Deposit Home Loans

Several government programs are designed to assist buyers with smaller deposits.

These include:

-

First Home Guarantee Scheme

-

Family Home Guarantee

-

Regional First Home Buyer Guarantee

These programs allow eligible borrowers to purchase property with a smaller deposit while avoiding lenders mortgage insurance.

Because eligibility rules apply, working with a mortgage broker can help determine which programs may be available.

Benefits of Low Deposit Home Loans

Low Deposit Home Loans provide several advantages for buyers entering the property market.

Enter the Property Market Sooner

Saving a 20% deposit can take many years. Low deposit home loans allow buyers to purchase property sooner and begin building equity.

Less Time Renting

Because the deposit requirement is smaller, borrowers may move from renting into home ownership faster.

Opportunity to Benefit From Market Growth

Entering the market earlier means borrowers may benefit from property price growth sooner.

Flexibility for First Home Buyers

Low deposit home loans for first home buyers often work alongside government grants and incentives.

Important Considerations With Low Deposit Home Loans

While these loans can be beneficial, there are important factors borrowers should consider.

Lenders Mortgage Insurance (LMI)

Most low deposit home loans require lenders mortgage insurance if the deposit is below 20%.

LMI protects the lender rather than the borrower and can increase the overall cost of the loan.

However, some borrowers may qualify for government schemes that remove this requirement.

Borrowing Capacity

Because the loan amount is higher relative to the property value, lenders assess borrower income, expenses and credit history carefully.

Interest Rate Considerations

Interest rates for home loans with low deposit may differ depending on the lender and risk profile.

Who Low Deposit Home Loans Are Best For

Low deposit home loans can suit a range of borrowers, particularly those looking to purchase property sooner.

They are commonly used by:

-

First home buyers entering the property market

-

Buyers with strong income but smaller savings

-

Professionals early in their career

-

Couples combining savings for a deposit

-

Buyers using government schemes

A mortgage broker can help determine which lenders offer the most suitable home loan low deposit options.

How to Apply for a Low Deposit Home Loan

Applying for a low deposit home loan typically involves several steps.

Step 1: Determine Your Borrowing Capacity

Understanding how much you can borrow helps determine your price range.

Step 2: Assess Deposit and Savings

Lenders will review savings history to confirm the deposit is genuine.

Step 3: Compare Lenders Offering Low Deposit Home Loans

Different lenders have different policies for:

-

deposit requirements

-

credit score

-

employment type

Step 4: Submit a Loan Application

Once a suitable lender is selected, the loan application can be submitted.

Step 5: Loan Approval and Property Purchase

Following approval, the loan proceeds to settlement once a property is secured.

Low Deposit Home Loans Melbourne Buyers Should Know About

For buyers in competitive property markets, low deposit home loans Melbourne borrowers access can provide a pathway into the market sooner.

Because property prices can change quickly, many buyers prefer entering the market earlier rather than waiting years to save a larger deposit.

Working with a mortgage broker can help identify lenders that support home loans with low deposit options suitable for Melbourne buyers.

Common Mistakes When Applying for Low Deposit Home Loans

Borrowers applying for low deposit home loans often make several avoidable mistakes.

Not Understanding Additional Costs

Many buyers focus only on the deposit and forget additional expenses such as:

-

stamp duty

-

legal fees

-

inspections

Choosing the Wrong Loan Structure

Loan features such as offset accounts, redraw facilities and fixed rates can influence long-term costs.

Applying With Only One Lender

Different lenders have different policies for low deposit home loans, meaning options can vary significantly.

Our Reviews

We pride ourselves on being brokers you can actually trust, from the initial consultation through to annual reviews that we perform years after your settlement, our tailored services and relationship focus is built to last.

Need proof that we are one of Melbourne’s best mortgage brokerages? Don’t just take our word for it – we have hundreds of positive Google reviews from real clients so you can rest assured you’re making the right choice with choosing Find A Better Rate Home Loans.

Frequently Asked Questions

Get in Touch

98% Approval Rate

18 Years Experience

18 Years Experience

98% Approval Rate

Latest Articles from Find A Better Rate

-

Is Refinancing Still Worth It in 2026? | Australia Guide

A Practical Australian Guide to Refinance Decisions Refinancing a home loan has never been just about chasing the lowest interest rate. It is a decision that involves costs, loan structure, lender rules, and your personal plans. In 2026, many Australian borrowers are reviewing loans taken out in a very different rate environment. At the same…

-

Aussie home owners just got $82,000 richer on average

What a way to start the new year! After a strong 12 months in the property market, plenty of homeowners around the nation are now a whole lot wealthier. And their newfound increase in home equity has opened up some exciting possibilities for 2026. Your home isn’t just a place to live in, it could…

-

Happy New Year! Let’s discuss some potential 2026 goals

There’s nothing quite like a New Year’s resolution to fire you up for another lap around the sun. Whether you’re looking to buy your first home, save on your mortgage, or leverage the equity in your current position, here are three resolutions to consider for 2026. So long, 2025 … You know what? We’ve got…

-

Is Refinancing Still Worth It in 2026? | Australia Guide

A Practical Australian Guide to Refinance Decisions Refinancing a home loan has never been just about chasing the lowest interest rate. It is a decision that involves costs, loan structure, lender rules, and your personal plans. In 2026, many Australian borrowers are reviewing loans taken out in a very different rate environment. At the same…

-

Aussie home owners just got $82,000 richer on average

What a way to start the new year! After a strong 12 months in the property market, plenty of homeowners around the nation are now a whole lot wealthier. And their newfound increase in home equity has opened up some exciting possibilities for 2026. Your home isn’t just a place to live in, it could…

-

Happy New Year! Let’s discuss some potential 2026 goals

There’s nothing quite like a New Year’s resolution to fire you up for another lap around the sun. Whether you’re looking to buy your first home, save on your mortgage, or leverage the equity in your current position, here are three resolutions to consider for 2026. So long, 2025 … You know what? We’ve got…

-

Season’s greetings! Here’s to a well-earned summer break

As the Christmas and New Year’s festive season rolls around, we want to take a moment to sincerely thank you for your trust and support throughout 2025. Fortunately, we had a bit more to smile about this year, with three RBA rate cuts and national property prices increasing by 8.7%. That said, 2025 wasn’t without its…

-

Is Refinancing Still Worth It in 2026? | Australia Guide

A Practical Australian Guide to Refinance Decisions Refinancing a home loan has never been just about chasing the lowest interest rate. It is a decision that involves costs, loan structure, lender rules, and your personal plans. In 2026, many Australian borrowers are reviewing loans taken out in a very different rate environment. At the same…

-

Aussie home owners just got $82,000 richer on average

What a way to start the new year! After a strong 12 months in the property market, plenty of homeowners around the nation are now a whole lot wealthier. And their newfound increase in home equity has opened up some exciting possibilities for 2026. Your home isn’t just a place to live in, it could…

Secure Competitive Home Loan Rates with Trusted Mortgage Lenders

Select from 35+ Trusted Lenders and Tailored Home Loan Solutions